While we know that Ren has definitely gone from his position as CEO and director of the club itself, there has been no confirmation of his departure from either Birmingham City Stadium Ltd (who own St Andrew’s) or from the strategic committee that was set up following the partial sale of Blues at the end of last year.

I’ve emailed the Birmingham Sports Holdings company secretary Robert Yam twice for confirmation that Ren has gone from these positions (as well as any other subsidiaries of BSH I might have missed) but have yet to receive a response. If and when I do, I will update this article.

However, Ren’s departure isn’t the only thing going on right now.

Last week BSH made a small announcement to the Stock Exchange of Hong Kong to confirm that rather than finding new projects to invest some money into, they were going to pay off some debt.

At the time of the announcement I thought this sounded quite positive and tweeted as such – after all, it makes sense not to waste money if there is nothing good out there, and paying debt off is always a good move.

However, while talking to someone else about the announcement to explain what was happening, I realised that there might be more to it than meets the eye.

So where was the money from originally?

The May 12 announcement makes it clear that the money was connected to a circular issued on November 17, 2020.

This can only be the circular sent to shareholders with regards to the sale of a stake in Birmingham City plc and Birmingham City Stadium Ltd to Oriental Rainbow Investments.

This is confirmed by this paragraph in the “Letter from the Board” section of the circular.

This confirmed that 60% of the money received was going to be used to pay debts that BSH owed to other companies; 20% to be used as working capital and 20% for investment in other projects.

As BSH confirmed in their May 12 announcement, they used HK$31.7M to pay off debts, and HK$10.5M for working capital. However they weren’t able to find any other suitable investments due to the ongoing COVID-19 pandemic and as such they made the decision to use the HK$10.5M left over to pay more debts off.

Who are these debts owed to?

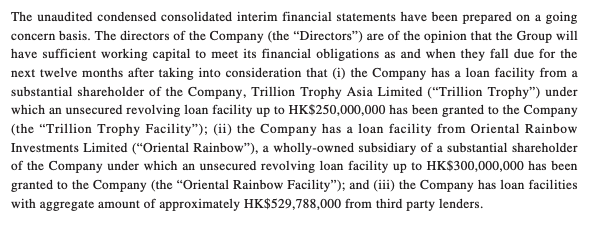

At the time of the original announcement we didn’t know exactly who BSH owed money to – and in truth, we only have a snapshot as of December 31 thanks to the interim accounts issued in February.

This paragraph in the interim accounts confirmed that there were three debts BSH had.

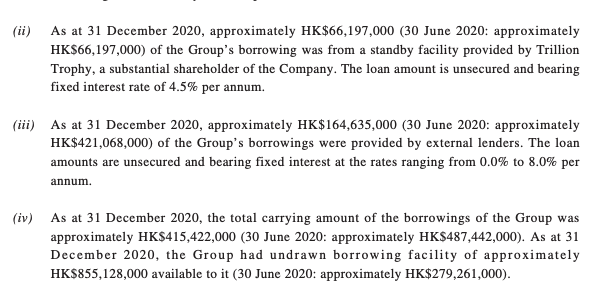

The first loan facility is owed to Trillion Trophy Asia and has been in place since BSH got relisted back in 2016. We can see from an entry further down in the accounts which confirms that BSH owes TTA HK$66.197M. This figure has been steady for some time now which suggests that TTA are in no hurry for it to be paid back and BSH are in no hurry to pay it back.

There is also confirmation that BSH owed HK$164,635,000 to “third party lenders” as of December 31, 2020.

We know from announcements in January that debts owed by BSH to two third party companies – Global Mineral and Join Surplus – were converted to shares.

The January 21 announcement confirmed that 1,062,576,000 new shares were created at a value of HK$0.13175 each. By multiplying the first figure by the second we can figure out how much money that paid off – a shade under HK$140M.

The announcement made on January 15 to initially confirm that deal stated that these shares were issued to wipe off debts BSH had to those companies.

That leaves one loan facility remaining that is outstanding from the interim accounts. That loan facility is for a total of HK$300M and has been granted by Oriental Rainbow Investments.

Now, it’s easily possible that BSH have opened a new loan facility with another company in the time span between the accounts being issued and now, but on the face of it this looks like a circular transaction.

The flow of it would appear to be:

ORI pays BSH a total of HK$52.7M for a 21.64% stake in Birmingham City plc.

BSH then uses at least HK$10.5M of that money to repay debt owed by BSH to ORI.

The best part of this transaction for ORI is that they didn’t just get 21.64% of the club; they also got 21.64% of the debt the club has to BSH. The interim report for BSH confirms that as of 31 December 2020 this stood at HK$222.6M.

Conclusion

If you’re struggling to follow all this, then don’t worry – it took me a week to understand the implications of the announcement.

Without referring back to previous parts of the deal it didn’t stand out at first but the more I thought about it and checked what I knew, the more it appears that ORI have bought a stake in Blues and got at least some of their money back straight off the bat.

I have to reiterate here though that I’m only going on the information available to me in the public domain and that there could easily be information that I’m not privy to which refutes what I have written above.

However, based on publicly available information it appears that there is a bit more to the transaction to sell a stake in Birmingham City than may initially appear to the eye.

I think people should also understand that transactions like this would appear to confirm my belief that the club would not be for sale to parties outside the current setup unless something drastically changes.

One thought on “BSH: Debt Transactions”

Comments are closed.